Authors

The flurry of policy related to price transparency and understanding the cost of care has continued into the new year. Last week, the president announced a Great Healthcare Plan (GHP) that looks to be a policy focal point in 2026. The fact sheet includes several elements that, if they were to become federal law, would continue to move the needle on accurately and efficiently guiding patients and employers towards a world where they should expect to know their costs of care upfront.

The reflections below highlight select elements outlined in the fact sheet aligned with areas we believe payers, providers, and innovators can work together to create a new world of minimized healthcare administrative friction that puts patient care back in primary focus. Let’s dig in.

Post Prices on the Wall

Within the hospital machine-readable files (MRFs), providers are already required to post their negotiated rates and cash pay prices for items and services offered. However, that cash pay rate requirement does not exist in payer MRFs, meaning the industry currently has a blind spot regarding cash prices for non-hospital care locations like imaging centers, labs, or ambulatory surgery centers. The GHP could address that gap in rate visibility through the requirement that “any healthcare provider or insurer who accepts either Medicare or Medicaid to publicly and prominently post their pricing and fees to avoid surprise medical bills.” Ideally any final language associated with this requirement specifically states cash pay rates must be included in the “pricing and fees” terminology.

Functionally, when a provider offers a limited list of services, such as a dermatologist or psychologist, a literal price list on the wall of the office and listed on the provider’s website is feasible. For hospitals though, short of unfurling a scroll of prices or creating a digestible list of standardized service packages (more on that further down in the blog), this requirement could be most helpfully accomplished through a patient estimate tool, good faith estimate, or advanced explanation of benefits (AEOBs). This is a prime opportunity for the government to tie in the No Surprises Act requirements to the GHP and provide a technical framework and enforcement plan for AEOBs and good faith estimates that require convening providers.

Create the “Plain-English Insurance” Standard

The fragmented claims billing, adjudication, and payment process that exists today is a major challenge toward the GHP’s call for health insurance companies and providers to “publish rate and coverage comparisons upfront on their websites in plain English—not industry jargon—so consumers can make better insurance purchasing decisions.”

Due to the complexity of clinical terminology, medical coding sets, and proprietary grouping software, patients and even subject matter experts who work in healthcare struggle to know with certainty what their total cost of care will be. Is one code sufficient to ascertain the cost of care? Or do you need multiple? And, if you do find you need multiple codes to reflect any upcoming medical or surgical service, how do you know which code impacts the final bill you’ll receive?

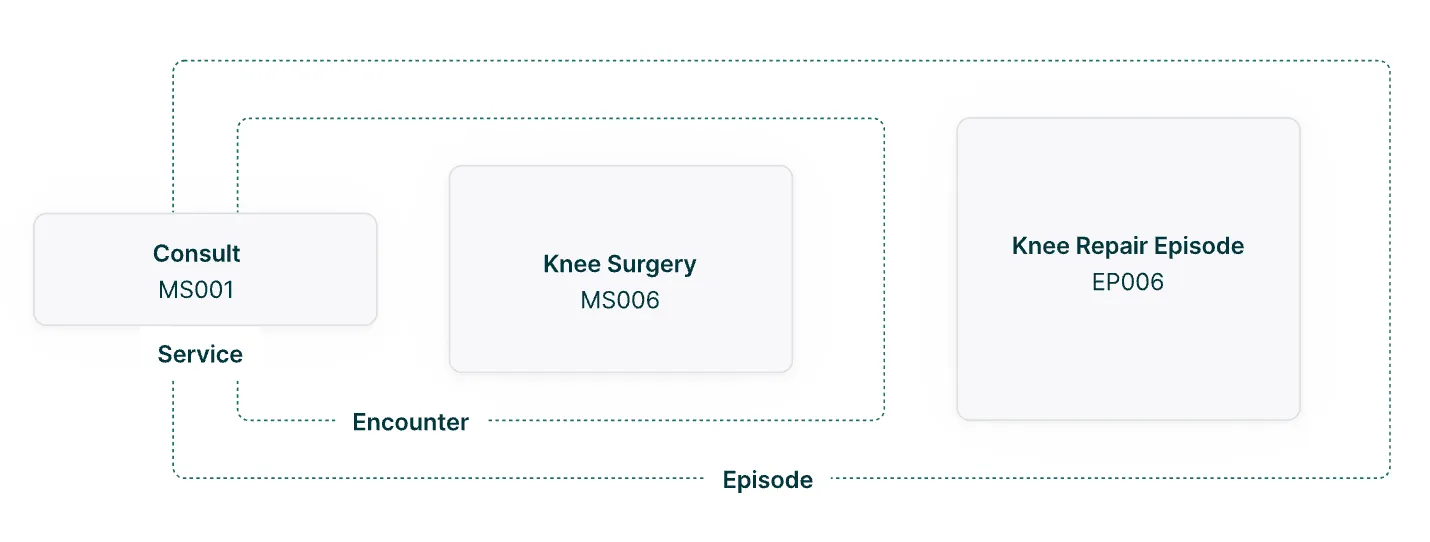

A major step toward answering these questions and using plain language within the billing ecosystem is an open-source approach to grouping claims to a single, digestible code. The PATIENTS framework that Turquoise is developing tackles this head on. From relatively simple visits with one provider to complex, multi-visit episodes of care, standard service packages (SSPs) consolidate all medical services, materials, and fees associated with a healthcare procedure into a single code. SSPs are open-source, patient-first, compatible with existing transaction standards and clearly distinguish between services, encounters, and episodes.

In order to provide plain language results for patients and employers, we believe a plain language SSP is foundational to creating this new standard.

Display Claim Rejection Rates

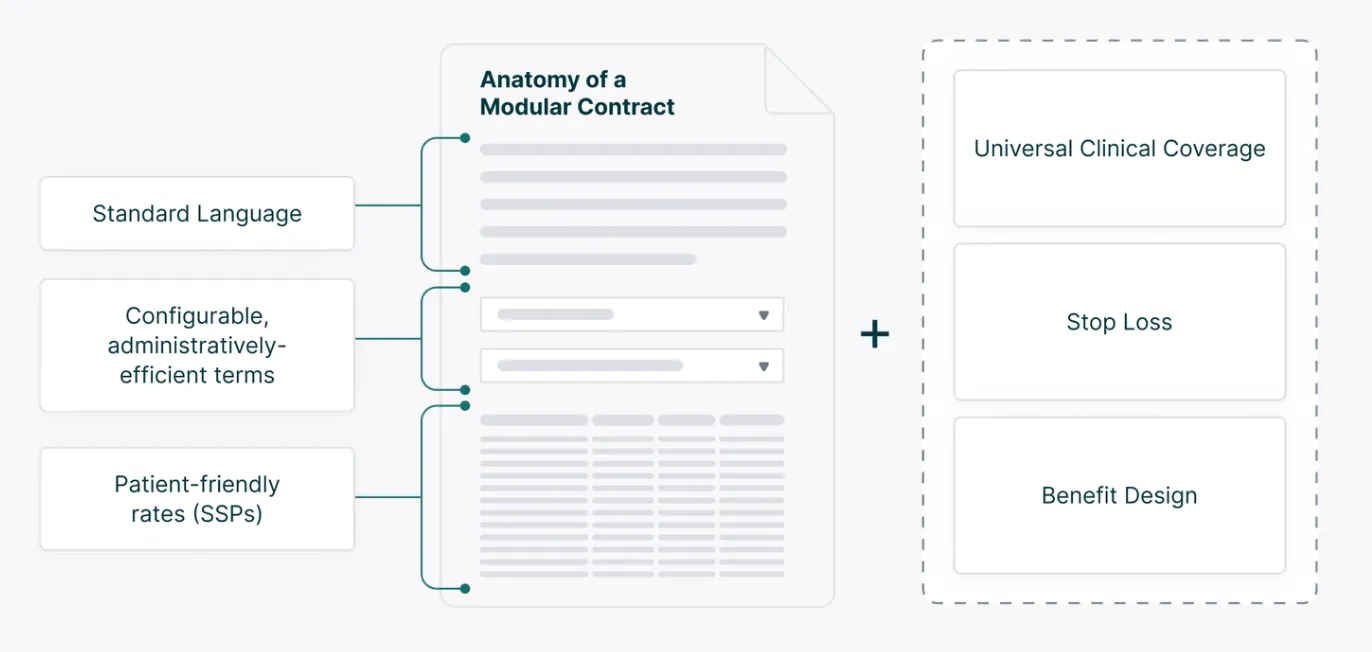

The language within the GHP is focused specifically on rejections (“Require health insurers to publish the percentage of insurance claims they reject”), but if we step back and look at the broader world of rejections, denials, or even clinical downgrades, we’re squarely in the quagmire of claims adjudication that wastes time, money, and resources for both providers and payers. Another element of the PATIENTS framework is modular contracts that would allow for a standard, re-usable formula for pricing a healthcare claim that combines industry standard provider-payer payment terminology.

The idea of a modular contract working alongside a universal clinical coverage library is incentivizing in a world where rejection rates are posted on websites or as an LED display on a billboard as you’re driving to receive care. Payers and providers both want high quality care delivery and healthy patients without so much time wasted on denials. One of the goals of our streamlined approach to coverage determinations and contracting is to meaningfully decrease the denials and rejections that currently plague the industry. In the world of the GHP, we believe this approach can and will allow payers to report that their rejections percentages are decreasing over time as new frameworks are adopted.

Turquoise Wishlist: The Codification of Requirements

Finally, as Turquoise has noted in previous public comments, the GHP presents yet another opportunity to codify requirements for payers and providers to publish contract information regarding high cost inpatient outlier rates. Patients will not typically seek out the negotiated rate for an outlier, because that care is not shoppable and/or any deductible or out-of-pocket amounts are generally met by the time outlier clauses kick in. However, for employers, high-cost outlier claims are a relatively small percentage of patients treated but a very high percentage of the cost of insuring an employee population. Employers will benefit from additional clarity that comes from reported outlier negotiated rates and the industry will get a better understanding of the full financial landscape of care when we know the cost of treating our sickest patients.

Much More on the Horizon

It’s exciting to see momentum continue to build towards transparency in healthcare prices and processes! We’ll be following any progress, updated guidance, and new requirements that come as a result of the GHP. If you’d like to work with Turquoise on the PATIENTS framework or have additional questions on policy, we’re always available to talk.

See inside the black box

Traceable data, unified workflows, and total transparency

Related resources

Learn, listen, and watch the latest on price transparency.

CMS’ new guidance puts stop loss on center stage

Celebrating official guidance on how to encode these complex terms into MRFs