Authors

Healthcare markets have historically been opaque. Secretive contracts were privately negotiated between payers and providers, with no single party having a complete understanding of the reimbursement landscape. Were different payers using fee schedules or negotiating a percent-of-charge, and for which services with which providers?

With price transparency data, we can finally get a comprehensive view of reimbursement structures in different care settings, across payers, services, and geographies. In Part One of this three-part series, we’ll examine how fee-for-service reimbursement structures vary across care settings and payers.

Digging in, we find that:

- Inpatient care is more often reimbursed at fixed rates

- Within each care setting there can be large differences in how each payer reimburses providers

- Aetna and Blue Cross have the most algorithmic rate contracts and allow more flexibility for providers to cover costs

- UnitedHealthcare and Cigna have the most fixed rate contracts and are best positioned to offer consumer-friendly price certainty

Reimbursement structure variation in contracts may reflect risk tolerance differences across care settings as well as market position differences between payers. Payers can use this data to understand where they stand in the market, and identify opportunities to create differentiated offerings for both consumers and providers. Before diving into these opportunities, we need to first understand the strengths of different reimbursement structures.

Reimbursement Structures: Fixed vs. Algorithmic Rates

Two distinct reimbursement philosophies dominate contracts: fixed rate reimbursement and algorithmic reimbursement. Through these reimbursement structures, payers not only shape hospital balance sheets but also impact how consumers shop for healthcare.

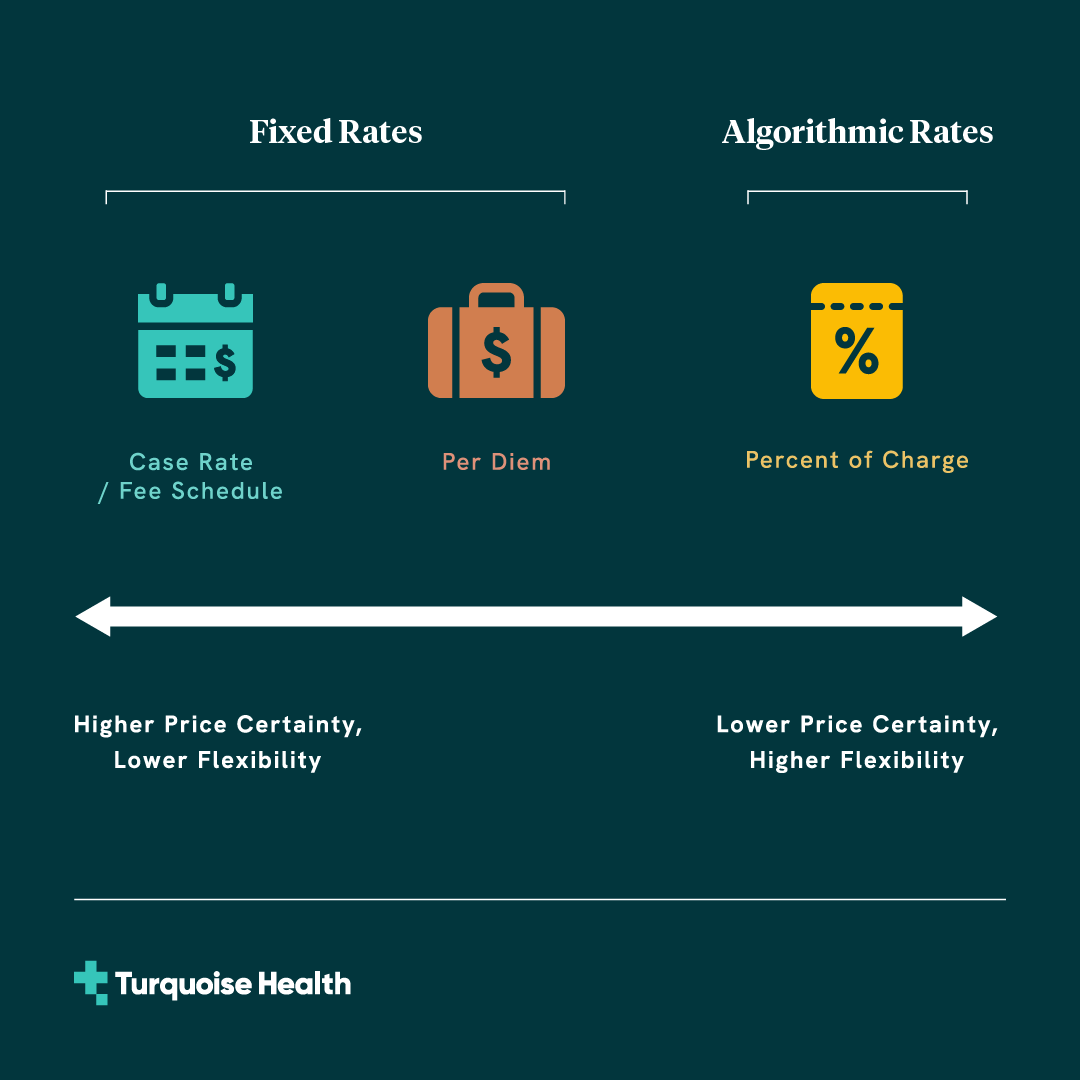

Fixed Rates

Under fixed rate reimbursement, payers establish predefined rates with providers for particular services.

- Reimbursement structures include case rates, fee schedules, and per diems*

- Provides consumer-friendly, upfront price certainty

- Leaves providers bearing the risk if their costs change

Algorithmic Rates

In contrast to fixed rates, algorithmic reimbursement create rates that require some calculation.

- Percent of charge reimbursement structure

- Provides flexibility for providers, allowing reimbursement to better align with the provider’s costs

- Introduces uncertainty for consumers, as final rates can only be calculated after care has been delivered

* Here we include per diem rates as fixed rates given that base amounts are negotiated as fixed dollar amounts. Because total costs for per diem rates exhibit some variability due to variation in length of stay, per diem rates can be considered somewhat of a hybrid between fixed and algorithmic rates, with moderate price certainty and moderate flexibility to align rates with provider costs.

In practice, many contracts blend fixed and algorithmic reimbursement structures to balance cost predictability and financial flexibility. For instance, payers may reimburse a hospital with a fixed rate for routine inpatient care, with separately negotiated percentages or carveouts for high-cost implants or procedures. Meanwhile, some outpatient services might have fixed rates, while others may be reimbursed based on a percentage of charge.

While this blending helps manage spend and risk across payers and providers, the complexity of these arrangements, unique payer-provider market dynamics, and closely guarded contracts have made it difficult for payers to get a holistic view of market standards. With CMS’ price transparency regulations and reporting standards, payers now have the ability to understand reimbursement structures across all contracts.

Reimbursement Variation Across Care Settings

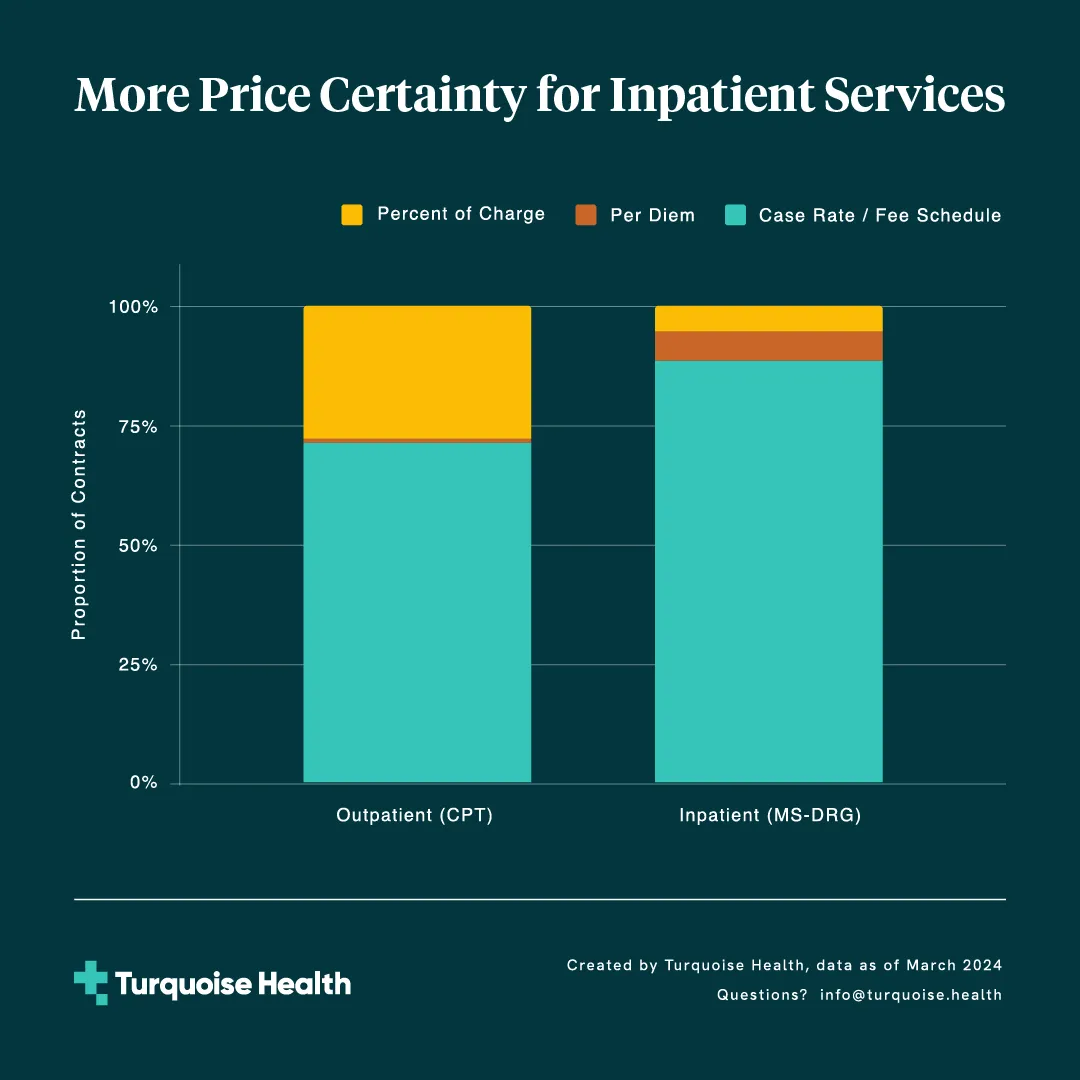

One of the clearest ways contracts segment rates is by care setting. Outpatient services are relatively limited in scope, can often be scheduled and planned in advance, and don’t require an overnight stay in the hospital. Given the predictable nature of these services, we might expect outpatient services to show more fixed rate price certainty and be easier for consumers to price shop. This expectation is reflected in CMS’ 500 shoppable services that were required to be included in payer patient estimate tools in 2023, as defined in Transparency in Coverage. Of the list, >99% are outpatient services.

But do outpatient services have enough price certainty to actually be shoppable? Across more than 10,000 outpatient services at over 5,000 general acute care hospitals, we find that 72% of outpatient rates are based on fixed rate structures, while a sizable 28% employ algorithmic rates. These algorithmic rates provide more flexibility for providers to cover their costs while introducing a layer of price uncertainty for consumers.

Inpatient services; however, show a different pattern. Here we focus on MS-DRG inpatient services, leaving inpatient revenue code rates for a future analysis. Looking at over 750 MS-DRGs across the same set of general acute care hospitals, we find that a large majority (95%) of these inpatient rates are reimbursed as fixed rates. This suggests a broader preference for predictable inpatient reimbursement, and indicates that MS-DRG rates may inherently provide appropriate levels of risk adjustment for providers to cover costs. The remaining 5% of inpatient rates are structured as percent of charge rates. Although the greater degree of contractual price certainty in inpatient services offers an opportunity for payers to pass along price certainty to members, these services are not easily shoppable.

Why are inpatient services reimbursed at fixed rates more often than outpatient services?

At first glance, this might seem surprising, since large-scope inpatient services can result in variable hospital costs that aren’t matched by fixed rates. In fact, fixed rates can be a valuable method for managing this variability. Given the complexity and variability of inpatient care, payers may prefer fixed rates as a form of risk sharing for these services. By agreeing on a case rate, payers know the maximum expenditure for a particular episode of care, while providers assume the risk of delivering all necessary services within that predetermined rate. The prevalence of fixed MS-DRG rates suggests that providers may find MS-DRGs and adjacent inpatient stop-loss provisions appropriately address population risk.

Another factor for reimbursement structure differences across care settings may be related to how different rates are contracted and reported. There are over 10,000 outpatient CPTs compared to just over 750 inpatient MS-DRGs. Many of these outpatient services are less costly than inpatient services, so they may not be explicitly negotiated. In these cases, the outpatient services may frequently fall under a contract’s catch-all percent of charge rate.

Regardless of the reason, the variation in reimbursement structure results in different market dynamics across care settings. The high prevalence of fixed rates for inpatient services provides payers more certainty on spend and is a strong starting point for passing along price certainty to their members. In contrast, the significant portion of algorithmic rates among outpatient services lets payers provide flexible reimbursement that helps providers cover their costs for these services. While reimbursement structure varies quite a bit across care settings, a closer look shows even more variation within care settings, between different payers. How are the major payers positioned?

Reimbursement Variation Across Payers

A closer look at the high-certainty rates of inpatient services shows some distinct differences between four national payers. For each payer we look across all inpatient services and break down the proportion of rates with each reimbursement structure. Cigna shows a particularly high prevalence of fixed rates, negotiating them in over 99% of their contracts. Aetna (99%) and UHC (98%) also show high levels of fixed rates. Blue Cross contracts, however, are more mixed, with fixed rates found in only 86% of inpatient agreements.

On the outpatient side, Cigna and UnitedHealthcare again demonstrate their focus on predictability, structuring 97% and 89% of hospital contracts with fixed rates, respectively. On the other hand, Blue Cross (69%) and Aetna (65%) have a lower proportion of fixed outpatient rates and relatively more percent of charge agreements.

Payer reimbursement structures can differ for a variety of reasons:

- Market Dynamics & Competition: The balance of power between payers and providers shapes contractual terms. In markets with concentrated provider systems, providers may have more leverage to push for percent of charge reimbursement that helps them better cover the variable costs of care. In contrast, payers with a strong market position can demand more predictable fixed rate agreements.

- Strategic Objectives: Payers’ strategic goals impact their preference for reimbursement models. Those focusing on cost predictability and spend may favor fixed rates, while others prioritizing high quality provider networks might opt for algorithmic rates to accommodate hospitals. This strategic choice reflects a payer's broader approach to market positioning, member satisfaction, and healthcare cost management.

In practice, contract reimbursement structures can be a complex mix of these and other factors. The differences in reimbursement structure and price certainty don’t just affect payer-provider dynamics but also have significant implications for members trying to understand their cost of care when scheduling an appointment.

An Opportunity for Differentiation

As we’ve seen, reimbursement structures vary quite a bit across payers, in different care settings. This variation reflects the different market positions and strategic objectives of each payer. Payers can use this information when considering how to best compete for consumers and providers.

Price transparency data shows that Aetna and Blue Cross+ have the most algorithmic rates, while UnitedHealthcare and Cigna have the most fixed rates. For Aetna and Blue Cross , prevalent algorithmic rates allow for provider-friendly flexibility for hospitals to cover costs, at the expense of price certainty for consumers. Appealing to providers by focusing on favorable reimbursement structures can help these payers quickly build attractive, differentiated provider networks.

For UnitedHealthcare and Cigna, prevalent fixed rates reduce flexibility for providers to cover costs, but also position these payers to offer consumer-friendly price certainty. In fact, we’ve seen UnitedHealthcare experiment in this area. In 2016 UnitedHealthcare created the Surest (initially called Bind) plan, which provided upfront pricing information to members in advance of treatment. UnitedHealthcare has reported strong consumer demand for this plan, perhaps an early signal of the consumer demand for price certainty.

Now that price transparency data is available, payers finally have the ability to understand how their contracts and reimbursement structures stack up. They can use this information to identify their competitive advantages and create differentiated offerings that better serve the distinct needs of consumers and providers. As the market continues to adapt to price transparency, we’ll be eagerly watching to see whether price certainty becomes a growing differentiator that payers offer members.

Methodology

Data

This analysis is based on the Turquoise Payer Dataset, which is derived from extracting, aggregating, and cleaning price transparency data from machine-readable files (MRFs) published by 200+ major health insurance companies. Payer Data contains negotiated rates for all covered services and procedures for each insurance company and insurance plan, reported monthly for all in-network healthcare providers. For this analysis, we limit the scope to March 2024 facility fees for the following payers, providers, and services:

- Payers: Aetna, Cigna, Blue Cross, and UnitedHealthcare.

- Providers: General acute care hospitals

- Services:

- Outpatient: all Current Procedural Terminology (CPT) codes

- Inpatient: all Medicare Severity Diagnosis Related Group (MS-DRG)

codes

Note that in some cases payers use custom code types (ie “CSTM-ALL”) in their MRFs. For example, UnitedHealthcare often uses this code type to report on outpatient facility fees. This analysis does not include these custom code types.

Analysis

Each contracted rate for a given payer-provider-service combination is mapped from the “negotiated_type” fields in the Transparency in Coverage files to reimbursement structures based on the following definitions:

- Case rate: ‘negotiated', 'fee schedule', and 'derived’ rates for MS-DRGs

- Fee schedule: ‘negotiated', 'fee schedule', and 'derived’ rates for CPTs

- Per diem: ‘per diem’ rates

- Percent of charge: ‘percentage’ rates

These contracted rates are then aggregated by care setting and by payer to calculate the proportion of contracted rates with each reimbursement structure.

See inside the black box

Traceable data, unified workflows, and total transparency

Related resources

Learn, listen, and watch the latest on price transparency.

CMS’ new guidance puts stop loss on center stage

Celebrating official guidance on how to encode these complex terms into MRFs